All Categories

Featured

Table of Contents

Keep in mind, nevertheless, that this doesn't say anything about adjusting for inflation. On the bonus side, also if you presume your option would certainly be to buy the stock exchange for those 7 years, and that you 'd obtain a 10 percent annual return (which is far from certain, particularly in the coming decade), this $8208 a year would certainly be greater than 4 percent of the resulting small stock value.

Example of a single-premium deferred annuity (with a 25-year deferment), with 4 settlement options. Courtesy Charles Schwab. The month-to-month payment here is highest for the "joint-life-only" choice, at $1258 (164 percent greater than with the instant annuity). Nevertheless, the "joint-life-with-cash-refund" option pays only $7/month much less, and warranties at least $100,000 will certainly be paid out.

The method you buy the annuity will certainly figure out the solution to that inquiry. If you purchase an annuity with pre-tax dollars, your premium minimizes your taxable income for that year. Eventual settlements (monthly and/or swelling amount) are tired as routine revenue in the year they're paid. The benefit here is that the annuity may let you delay tax obligations past the internal revenue service contribution restrictions on Individual retirement accounts and 401(k) plans.

According to , purchasing an annuity inside a Roth plan leads to tax-free repayments. Getting an annuity with after-tax dollars beyond a Roth results in paying no tax on the part of each settlement credited to the original costs(s), however the staying part is taxable. If you're setting up an annuity that begins paying prior to you're 59 years old, you may need to pay 10 percent early withdrawal penalties to the internal revenue service.

What is the best way to compare Guaranteed Income Annuities plans?

The expert's initial step was to create a detailed financial prepare for you, and then clarify (a) exactly how the suggested annuity suits your overall plan, (b) what alternatives s/he thought about, and (c) exactly how such choices would certainly or would not have actually caused reduced or greater settlement for the advisor, and (d) why the annuity is the premium selection for you. - Annuities for retirement planning

Obviously, an advisor may try pushing annuities even if they're not the best fit for your situation and goals. The reason could be as benign as it is the only item they sell, so they fall prey to the typical, "If all you have in your tool kit is a hammer, pretty quickly everything begins resembling a nail." While the expert in this circumstance may not be underhanded, it enhances the danger that an annuity is a poor selection for you.

Where can I buy affordable Tax-deferred Annuities?

Because annuities commonly pay the representative selling them a lot higher compensations than what s/he would obtain for spending your cash in mutual funds - Flexible premium annuities, let alone the zero compensations s/he would certainly receive if you spend in no-load mutual funds, there is a huge reward for agents to push annuities, and the more difficult the better ()

A deceitful consultant suggests rolling that amount right into brand-new "much better" funds that just occur to bring a 4 percent sales load. Accept this, and the consultant pockets $20,000 of your $500,000, and the funds aren't likely to carry out far better (unless you chose much more poorly to start with). In the exact same example, the consultant could steer you to acquire a complex annuity keeping that $500,000, one that pays him or her an 8 percent commission.

The expert attempts to hurry your choice, claiming the offer will certainly soon go away. It may certainly, however there will likely be similar offers later on. The expert hasn't figured out how annuity settlements will be taxed. The expert hasn't revealed his/her settlement and/or the charges you'll be billed and/or hasn't shown you the effect of those on your eventual settlements, and/or the settlement and/or costs are unacceptably high.

Your family history and present health point to a lower-than-average life span (Long-term care annuities). Current passion prices, and hence projected settlements, are traditionally reduced. Even if an annuity is best for you, do your due persistance in contrasting annuities marketed by brokers vs. no-load ones offered by the issuing business. The latter may need you to do even more of your own research study, or use a fee-based economic expert who might receive payment for sending you to the annuity issuer, but might not be paid a higher payment than for other financial investment choices.

How long does an Lifetime Income Annuities payout last?

The stream of monthly settlements from Social Security is comparable to those of a deferred annuity. A 2017 relative evaluation made a thorough contrast. The adhering to are a few of one of the most salient factors. Because annuities are voluntary, individuals purchasing them generally self-select as having a longer-than-average life span.

Social Safety benefits are totally indexed to the CPI, while annuities either have no rising cost of living protection or at the majority of offer a set percent annual boost that may or may not make up for rising cost of living in full. This kind of motorcyclist, as with anything else that increases the insurer's threat, requires you to pay even more for the annuity, or accept reduced settlements.

What is the difference between an Variable Annuities and other retirement accounts?

Please note: This write-up is planned for informative functions only, and need to not be taken into consideration financial guidance. You need to consult a monetary specialist prior to making any kind of significant monetary decisions.

Given that annuities are planned for retirement, tax obligations and penalties may use. Principal Security of Fixed Annuities.

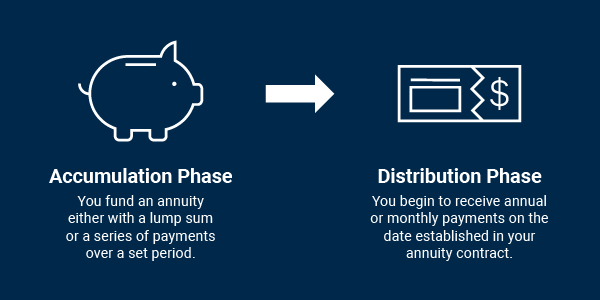

Immediate annuities. Used by those that want trusted earnings quickly (or within one year of purchase). With it, you can customize income to fit your needs and develop income that lasts for life. Deferred annuities: For those who intend to expand their money in time, however are eager to postpone access to the cash up until retirement years.

How do I cancel my Deferred Annuities?

Variable annuities: Gives better possibility for growth by investing your cash in investment alternatives you select and the capacity to rebalance your profile based upon your preferences and in such a way that aligns with changing financial goals. With fixed annuities, the company spends the funds and offers a rates of interest to the customer.

When a fatality case accompanies an annuity, it is essential to have a named beneficiary in the agreement. Various alternatives exist for annuity survivor benefit, relying on the contract and insurance company. Selecting a reimbursement or "period specific" alternative in your annuity provides a survivor benefit if you pass away early.

What is the difference between an Tax-deferred Annuities and other retirement accounts?

Naming a recipient other than the estate can aid this procedure go much more smoothly, and can help make sure that the earnings most likely to whoever the individual wanted the cash to visit instead of going via probate. When present, a death advantage is automatically consisted of with your agreement. Depending upon the type of annuity you acquire, you might have the ability to include enhanced survivor benefit and features, yet there could be added prices or fees related to these add-ons.

{kind=link}

Table of Contents

Latest Posts

Decoding How Investment Plans Work Everything You Need to Know About Financial Strategies Breaking Down the Basics of Fixed Income Annuity Vs Variable Growth Annuity Advantages and Disadvantages of An

Breaking Down Variable Annuities Vs Fixed Annuities A Comprehensive Guide to Investment Choices Defining Fixed Vs Variable Annuities Advantages and Disadvantages of Tax Benefits Of Fixed Vs Variable A

Analyzing Strategic Retirement Planning Key Insights on Variable Annuities Vs Fixed Annuities Defining the Right Financial Strategy Advantages and Disadvantages of Different Retirement Plans Why Fixed

More

Latest Posts